Any developing economy’s government's Mission is to expand its export. The rationale for the same is to maintain the balance of payments, create jobs and boost the economic growth.

By providing certain benefits and reliefs on exports, the government promotes the trade. The exporters can avail these benefits and reliefs and thus undertake a free-flowing and beneficial trade. On the same notes, the government provides certain benefits under the GST regime to exporters.

Thus, there is no incidence of the tax (net effect) in a case where an exporter export goods/services from India.

Under GST regime, the exporter has either of the two options:

- Export under bond without payment of tax

- Export along with tax payment and claim refund later

Here we give an insight into the details about when to opt for LUT and when to opt for Bond. Not only this but also how to claim the refund of IGST paid on exports in simple steps.

In this article, We cover the following:

Brief on refund of IGST paid on Exports

Under GST laws, the exporter has option to pay IGST on exports and then claim refund of the same. The process of claiming refund has been made easy for the export dealers. For export of goods or services or both, there is no need to file refund application (GST RFD-01) separately. The shipping bill filed by the exporter is a refund claim in itself. (Please refer to the next section 3.0 for an insight into the details to be furnished)

The exporter charges IGST on the invoice for export at the applicable rate (rates specified for different goods and services). On payment of IGST the refund can be claimed for the following two elements:

- Input tax credits on goods and services which remained unutilised;

- IGST paid on export of goods or services.

The law specifies that shipping bill is to be considered as a refund claim on satisfying following two conditions.

- The person carrying export goods should file an export manifest and

- The applicant should have filed the returns GSTR-3 or GSTR-3B appropriately. A refund is initiated on filing table 6A in Form GSTR-1.

On filing the above documents appropriately, the refund is processed by the department.

Steps for claiming refund of IGST paid on Exports

Learn how to access, add details and file Table 6A in GSTR-1 using our detailed guide.

The details as entered in Table 6A should match the details of invoices and shipping bill uploaded on ICEGATE portal by exporters.

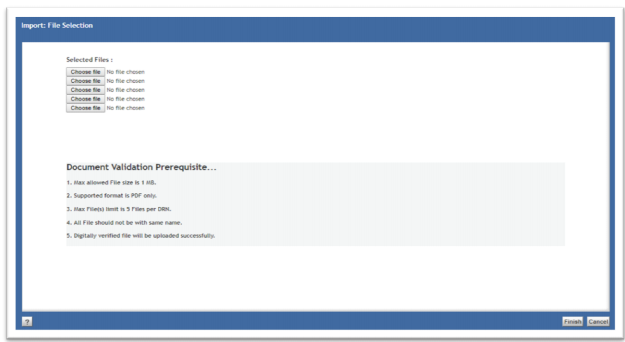

The steps to upload documents on the ICEGATE portal is as follows:

Step-1: Prepare documents in specified formats (PDF) for upload to the portal

Step-3: Go to e-SANCHIT tab for uploading the documents.

Step-4: Click on the upload documents button. At a time, a batch of maximum 5 documents can be uploaded.

Step-5:

Select export documents to be uploaded from the drop-down list. All the documents should be digitally signed before uploading.

Step-6: Validate the DSC on the documents by clicking on Validate Document button for each document.

Step-7: Click on submit documents. Click the OK button on a disclaimer that will appear to accept the responsibility for the genuineness of the documents uploaded.

Step-8: On successful submission, a unique IRN number will be generated which can be used for future reference.

When to file form RFD-01 / RFD-01A (for tax refund in case of exports)

The excess of unutilised ITC (Input Tax Credit) can be claimed by way of filing Form GST RFD-01 (for online filing) / GST RFD-01A (for manual filing). A simple form is to be filled and filed accordingly with the department for claiming such refunds or any amount paid by mistake or the excess of amount lying in cash ledger.

The following details are to be filed in:

- The GSTIN/ Temporary ID allotted

- Legal name

- Trade name (if any)

- Address of the principal place of business

- Tax period for which the claim of refund is made (if applicable)

- Amount of IGST, CGST and SGST, Interest or cess (if any)

- Grounds for the claim of refund (as per the list given)

- Details of Bank account in which the refund is to be credited

- Select ‘Yes’ if the document required to be submitted in Annexure 1 for the reason selected at (vii). Else select ‘No’

- Verification: To be signed by the authorised person

Certain time limits and frequencies of filing Form GST RFD-01/01A have been prescribed as under:

Time limits: The Form RFD-01/01A has to be filed within a span of two years from the relevant date.

Frequency of filing: The Form RFD-01/01A has to be filed on a monthly basis by exporters.

Within 15 days of filing such refund application, the officer assess for and verifies the completeness and correctness of all the details provided. Form RFD-02 is made available as an acknowledgement of the application filed. If any details are missed or incorrect, the assessing officer will intimate the exporter through Form RFD-03 which shall be updated and refiled. While processing the refund claim of unutilised ITC, the value of goods declared in GST invoice and the value in corresponding shipping bill/bill of export is examined and if both are different, then lower of the two values is sanctioned as a refund.

In a scenario where the exporter is undertaking the export by furnishing a Bond, he/she need not pay taxes on such sale.

What is Letter of Undertaking (LUT) and Bonds

Letter of Undertaking (LUT)

It is a type of bank guarantee, under which a bank allows its customer to raise money from another Indian bank’s foreign branch as a short-term credit.

The purpose of such undertakings is to ensure that owner of the ship or aircraft would:

- employ security on the vehicle;

- enter an appearance acknowledge ownership;

- pay any final decree entered against the vehicle whether it is lost or not.

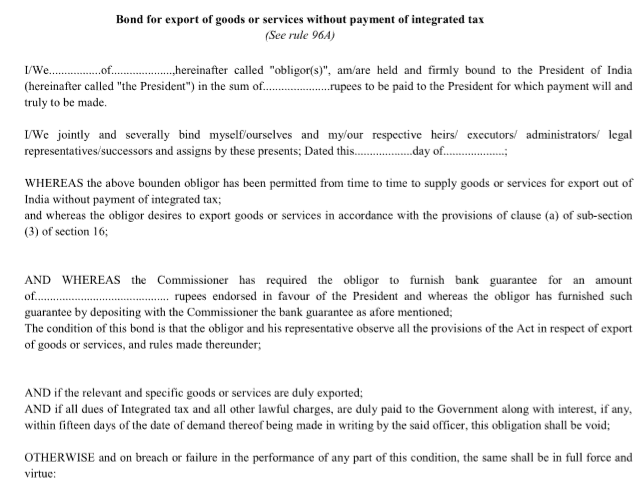

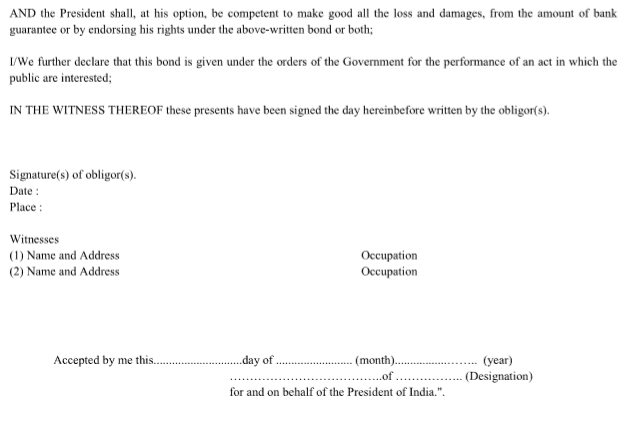

Bonds

It is a financial instrument in which the issuer of bond owes the holders a debt and is obliged to pay them interest or to repay the principal at a later date. It is a highly secured and highly liquid financial instrument which is mostly negotiable. This means that the ownership of the bond can be transferred. The most common types of bonds are municipal bonds and corporate bonds.

In case of furnishing bonds for exports, the general parlance is B-1 Surety / Security (General Bond) is furnished. These kinds of bonds have a surety (another person) who guarantees the performance on the part of the obligor (person furnishing the bond).

Who can use Letter of Undertaking (LUT) and Bonds for exports

Any registered taxpayer exporting goods can make use of LUTs. However, any person who has been prosecuted for tax evasion for an amount of Rs. 2.5 Crores or above under the act is not eligible to furnish LUTs.

The validity of such LUT’s is for a period of one year (till the end of financial year). An exporter furnishing LUT’s are required to furnish fresh LUT for each financial year. If the conditions mentioned in LUT are not satisfied within the time-limit, the privileges are revoked and the exporter will have to furnish bonds.

For all the other assesses (along with the ones who have been prosecuted for tax evasion of Rs. 2.5 Crores or above under the GST laws), bonds should be furnished if the export is being made without payment of IGST.

The Letter of undertakings can be furnished and submitted online through the GST portal (refer 7.0 for steps to furnish LUT’s). At the same time, the bonds are required to be furnished manually as the hardcopy of the same has to be remitted to the department.

Example of transactions for which LUT/Bonds can be used:

- Zero-rated supply to SEZ without payment of IGST

- Export of goods to a country outside India without payment of IGST

- Providing services to a client in a country outside India without payment of IGST

What happens if goods or services are not exported?

As per the specifications laid in Rule 96A of the CGST Rules,

- The exporter shall be liable to pay taxes, with interest if:

- Goods are not exported outside India within 3 months of issuing the export invoice tax should be paid within 15 days from the end of such three months period);

- On a failure to render services or if the payment for goods is not received in convertible foreign exchange within one year then within 15 days from the expiry of such one year.

- Form GSTR-1 with details of invoices of export shall be filed with a confirmation of goods have been exported out of India

- If the goods are not exported and the assessee does not makes the payment accordingly, the amount shall be recovered as described in the act (Section 79) and the export is withdrawn.

- As soon as the payment is made, the exports are restored. Also in cases where the exports take place after three months, the benefit is restored.

How to file Letter of Undertaking (LUT) and Bonds for exports

Below are the steps on how to file and furnish Bonds in the case where the exports are made without payment of taxes:

Step 1: Check the furnishing requirements (Whether LUT is to be filed or Bond) and jurisdiction. If a Bond is required to be filed then additional documents relating to bank guarantee is also required to be prepared.

Step 2: Prepare necessary documents for Bonds. Following documents are to be filed for bonds:

For Bonds:

- Form RFD-11 on letterhead

- Bond on stamp paper

- Bank guarantee

- Authority letter (For example, if the bond is signed by the MD of a company then a copy of Board Resolution authorising him to act on behalf of the company is required to be furnished)

- Other supporting documents.

The exporter need not furnish a separate bond for each consignment. Instead, he can furnish a Running Bond. When using a Running bond, the exporter carries forward the same terms and conditions in the bond for the next consignment. Say if an exporter furnishes a Running bond of Rs. 2 Crores, then he can export goods worth of taxes to the tune of Rs. 2 Crores in multiple transactions. On fulfilling the conditions in the bond, the amount is freed up and can be used for next transactions for export.

Step 3: Along with an office copy, a duplicate copy of the above shall be prepared.

Step 4: Submit the documents to the department and get the same verified from the relevant officer to avoid any rejections and resubmissions.

Step 5: Within 2 to 3 days of filing the documents, a signed letter shall be issued by the officer acknowledging the same.

Format of LUT and Bonds in RFD-11

The Form RFD-11 is filed in the format below:

Form for LUT:

- Registered Name

- Address

- GST No.

- Date of furnishing

- Signature, date and place

- Details of witnesses (Name, address and occupation)

Format of Letter of Undertaking (LUT) and Bond is as given below

Form for Bonds:

- Registered Name

- Address

- Amount of bond furnished

- Date of furnishing

- Amount of bank guarantee furnished

- Signature, date and place

- Details of witnesses (Name, address and occupation)